BLUEPRINT FOR A COMPANY IN AMERICA 2.0?

On March 2, VectoIQ Acquisition Corp. (VTIQ) proposed to combine with Nikola Motors, a company focused on the development of next-generation smart transportation. Upon the closing of the transaction, the combined company will be named Nikola Corporation and remain NASDAQ-listed under the new ticker symbol “NKLA.”

Nikola’s business plan is to be a vertically integrated zero-emissions transportation solution provider. Nikola’s core product offering centers around its battery-electric vehicle (“BEV”) and hydrogen fuel cell electric vehicle (“FCEV”) Class 8 semi-trucks.

Essentially, they are Tesla for Trucks. A bold visionary/disruptor, Trevor Milton (Executive Chairman), has been able to problem-solve for a fair amount of issues that arise when thinking about a “greener” path for the transportation sector and Hydrogen’s role. Fuel-cell batteries have been lauded as a good option for long-haul routes in trucking. Still, infrastructure build-out for fueling purposes has been a significant hurdle for industry adoption.

Why hydrogen fuel cell over battery-electric, you ask? Hydrogen Fuel Cell technology has been called “fool cells” by Elon Musk, and when comparing the two technologies, it does look like BEVs make more sense for the Auto market as well as the short-haul market. The charging infrastructure is more established for BEVs, just plug it into the electric grid. To be a vehicle fuel, hydrogen needs to be produced. That process takes energy, and most of the methods of production have some relationship with fossil fuels or natural forms of greenhouse gases. Kind of defeats the purpose, right? Now, there is one method that, if designed right, can be as near to a carbon-free fuel as there is. If one can harness wind and/or solar energy, use that energy to produce hydrogen from water by electrolysis and then fuel a vehicle onsite (eliminating the transportation issue), you could claim a zero-carbon solution.

I don’t see that happening for the auto market as the infrastructure build-out needed would be too large. However, hydrogen has a distinct advantage when it comes to the long haul market. Between refueling, FCEVs can travel farther than BEVs. A Class 8 BEV has a top range of 300 miles, though the Tesla Semi claims a range of 500 miles, and the electricity draw, as well as the weight of the batteries needed, are problematic as well. FCEVs can travel farther between charges, and the fuel cell stack is apparently more efficient weight-wise than BEVs. Nikola is presenting a truck with a range of 500 to 750 miles, which is on par with today’s diesel trucks. Other differentiators that favor FCEVs over BEVs are shorter fueling times and reliability to operate in cold weather.

The opportunity in front of them is tremendous. Globally, the commercial vehicle market, is estimated to be ~$600 billion-per-year (Source ACT Research) with steady growth expected to continue as e-commerce and global economic growth fuel the need for more heavy-duty trucks. According to ACT, expectations are for ~5% annual growth in the Class 8 truck population from 2019 to 2023, driven by double-digit yearly growth in e-commerce and a healthy global economic outlook. Now, of course, this past month probably puts these numbers in jeopardy of being revised down or hopefully pushed out in time.

Combine the above with the push to reduce greenhouse gas (GHG) seen across the globe, and the market opens up even more for Nikola. According to the International Council on Clean Transportation (ICCT) heavy-duty trucking in the U.S. and EU, which is <10% of the vehicle population, is responsible for ~40% of GHG from the transportation industry.

Before the pandemic, there was a tremendous push to reduce global GHG emissions from leading governments. For example, the EU has a mandatory 15% reduction in CO2 emissions by 2025, and a 30% reduction target by 2030. To incentivize industry players, they have put in place financial penalties for failure to achieve these targets. Conventional technology (diesel) will most likely have trouble helping companies meet the EU targets. And this is where Nikola can come in. As they eloquently put it in their filing, “These ambitious CO2 targets are likely ‘technology-forcing’ towards alternative powertrains such as battery-electric and hydrogen fuel cell.” In the U.S., states have put in place a bevy of incentives for producers to pursue non-fossil fuel endeavors.

The company openly states that the economics rely on federal and state grants, loans, and tax incentives under government programs designed to stimulate the economy and support the production of alternative fuel and electric vehicles and related technologies, as well as the sale of hydrogen. Before the pandemic, these initiatives were well entrenched in the investment decision-making of companies and lenders, both private and public. I think we can all safely say that the investment landscape is currently in a state of violent flux, and programs rooted in forecasting financial models might be in jeopardy. The details of the Coronavirus Aid, Relief, and Economic Security Act (CARES) do not specifically address the next phase of the U.S. economy but it is clear that there will be federal government role in rebooting the economy and lobbyists are surely already jockeying for a seat at that table.

I can’t imagine the ravaging the current state of affairs is having on state budgets, and what they are going to do once we get through this will be up for debate probably for years. It is my opinion that the Green New Deal was absurd and impossible to implement. But, I did and still do believe that aspects of a green new deal (notice the lowercase) will be a part of “America 2.0 – the rebooting”.

The undertaking that Nikola presents, particularly the build-out of 70 hydrogen stations by 2028, is a crucial part of the narrative. I can say that companies like Nikola should be a part of a “new” America, but I am not sure if that is the route our leaders will take us.

So, the backdrop for Nikola was promising as they position themselves as a company that can provide the balance of economic solutions for corporations attempting to become greener without losing financial returns. One can argue on the merits of government intervention in a “free market,” but the push was there.

I have followed the energy space for many years, and I have seen transformative events change the flow of investment in numerous ways and directions.

The conventional gave way to the unconventional, and it looked like the baton was passing to the renewable. Now the race has been postponed.

Nikola Motor Corporation

The slide presentation accompanying the merger announcement shows the blueprint the company intends to use as it matures into a going concern. They address a fair amount of the issues I have seen with alternative fuel initiatives in the past. Infrastructure build-out, commodity cost exposure and early adoption risks in particular.

A crucial part of the business plan is to build out a network of hydrogen fueling stations. Another feature that is of note is the offering of a bundled lease. This approach should provide customers with a FCEV truck, hydrogen fuel, and maintenance for a fixed price per mile. The Nikola model addresses the early adoption risk by initially partnering up with companies with dedicated routes.

This approach allows customers to lock in a fuel price, which in the conventional diesel world can be highly variable. The fixed-rate also helps Nikola’s ability to de-risk infrastructure development as they can lock in end-user demand and map capital outlay accordingly.

CONSIDERATIONS

As a non-revenue generating company, there is going to be a fair amount of risks, and for investors and potential investors here are some things to consider:

- They are not registered as a dealer in any state, and many States prohibit manufacturers from selling vehicles directly to customers.

- As a company, they do not have experience in high volume manufacturing. However, they have partnered with CNHI Iveco, a leading manufacturer of trucks, buses, and light commercial vehicles in Europe.

- Though they have reservations for 14,000 Nikola Two FCEV trucks, they do not have lease agreements. I think the arrangement with AB Inbev for 800 vehicles is particularly vital as the hydrogen filling station buildout looks to be hand in hand.

- The corporations on the bottom right of slide 13 are all well-known names and it was pointed out to me that most of them are not unfamiliar with hydrogen fuel-cell vehicles as most of their fork-lift fleets are FCEVs.

- They plan on using a third-party partner to provide financing to their prospective customers.

- Competition is intense with Daimler, Hyundai, Tesla, Toyota, and Volvo, all working on BEV and FCEV trucks. Looking at the timelines of the competitors it does not seem like anyone has a first mover advantage at the moment.

FINANCIALS

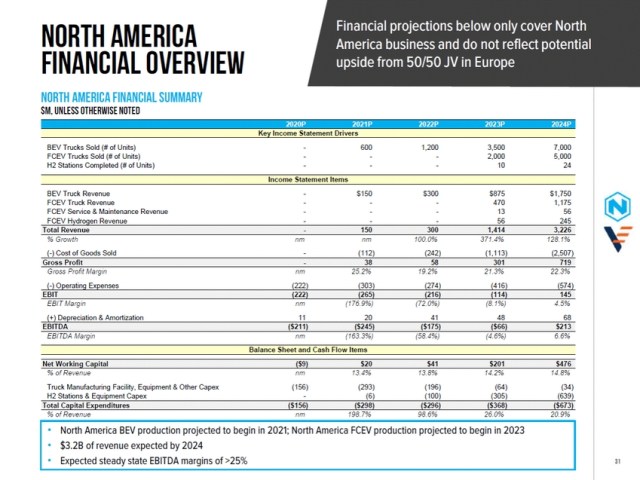

At closing, the company is expected to be nearly debt-free and have over $700 million in cash. On slide 31 of the presentation, they put together projections for the years 2020 – 2024, and it looks like they will need to raise another $1.5 billion over that period to support their goals.

I would be incredibly impressed if they don’t revise the timelines presented for their BEV truck (slide 28) and FCEV truck (slide 29) roll-outs.

But, if they do, I would assume the investor base would accept it. I am not well-versed in the world of bringing vehicles to market but, I did find the timelines to be very ambitious, especially considering they have not broken ground on their manufacturing facility in Arizona.

For valuation, it looks like they are pointing investors to 2027 metrics as truck revenues are estimated to be above $10.5 billion and EBITDA to equal $1.35 Billion.

These numbers do not include the contributions of the H2 stations or the Europe JV.

To DOWNLOAD the report click:

VECTOIQ/NIKOLA COMBINATION REPORT

To contact Mike McAllister by email:

Disclaimer: This note has been prepared by SPACInsider.com for informational purposes only and is not a solicitation of any offer to buy or sell any security or to participate in any trading strategy. THIS IS NOT INVESTMENT RESEARCH OR INVESTMENT ADVICE – each investor should conduct their own independent analysis of the instrument or trading strategy and request all information they require to make their own investment decision, including, where applicable, a review of any prospectus, prospectus supplement, offering circular or memorandum describing such security. The information contained in this Note has been obtained from public sources and such information is believed to be correct and reliable but has not been independently verified. SPACInsider does not make any guarantee, representation, warranty or undertaking, express or implied, as to the fairness, accuracy, reliability, completeness, adequacy or appropriateness of any information or comments contained in this Note. Furthermore, the information may not be current due to, among other things, changes in the financial markets or economic environment. SPACInsider has no obligation to update any information contained in this Note. Any reference to past performance should not be considered indicative of future performance. Unless otherwise stated, all views or opinions herein are solely those of the author(s) as of the date of publication, are subject to change without notice, and are published for the general information of recipients, but are not to be relied upon as authoritative or taken in substitution for the exercise of judgment by any recipient.

Despite a week of general pull-backs in the market, fintech firm Ibotta (NYSE:IBTA) nonetheless took the dive and had a good week debuting via a traditional IPO in the choppy waters. The company, which provides app-based consumer cashback discounts on purchases, priced its IPO at $88, above its proposed range of $76 to $84, and...

At the SPAC of Dawn Happy Friday! SPACInsider has unveiled new presets on SPAC Performance accessible via the Data drop-down to easily sort for the highest and lowest performing active SPACs and de-SPACs. On the de-SPAC side, Vertiv (NYSE:VRT) continues to be well ahead of the pack, logging a 710% return by share price adjusted...

AGBA (NASDAQ:AGBA) stock is up over +90% this morning following a +211% premarket spike on news it has signed a definitive agreement to combine with social streaming video platform Triller. AGBA, the company itself, was formed by the $555 million combination between a SPAC of the same name and TAG Companies, a financial services firm...

At the SPAC of Dawn Since closing its combination with DHC last month, AI customer engagement firm BEN (NASDAQ:BNAI) has rolled out new partnerships with call center and healthcare clients. And, while it faces a fair bit of competition in the chatbot realm, several high-profile institutions have demonstrated that creating one that provides useful services...

Blue Ocean (NASDAQ:BOCN) provided significantly more texture today in the presentation for its $275 million combination with Asian digital media group TNL Mediagene, which it expects to hit profitability in the second half of the year despite a slight shakeup in financing for the transaction. The first big update in the first investor deck is...