Friday evening saw Act II Global Acquisition Corp. file for a $250 million SPAC IPO and it was the first new SPAC filing in roughly three weeks. SPACs come in waves, so if the past is any indicator, expect a few more new filings in the next week or two to give Act II a run for their money (literally).

However, we have yet another 100% in trust, 24 months, 1/2 warrant deal, planning to raise $250 million. It’s a little curious because SPACs are known for both evolving the structure and providing a variety of different options of that structure. It’s not uncommon to see three deals price in one week where one SPAC offers a right, one offers 18 months with 1 warrant, and another with 24 months and 1/2 or 1/3 warrant, all at different capital raise levels. Yet since March 1st, the deal structures have looked remarkably similar.

| SPAC | Initial Filing Size ($mm) | Warrants | % in Trust | Date of IPO | |

|---|---|---|---|---|---|

| 1 | Act II Global Acquisition Corp. | 250.0 | 0.5 | 100% | TBD |

| 2 | Iswill Acquisition Corp. | 230.0 | 0.5 | 100% | TBD |

| 3 | B. Riley Principal Merger Corp. | 150.0 | 0.5 | 100% | TBD |

| 4 | Replay Acquisition Corp. | 250.0 | 0.5 | 100% | April 4, 2019 |

| 5 | 8i Enterprises Acquisition Corp. | 50.0 | 1 for 0.5 | 100% | March 28, 2019 |

| 6 | Insurance Acquisition Corp. | 130.0 | 0.5 | 100% | March 20, 2019 |

| 7 | Trine Acquisition Corp. | 250.0 | 0.5 | 100% | March 15, 2019 |

| 8 | Crescent Acquisition Corp. | 250.0 | 0.5 | 100% | March 8, 2019 |

| 9 | Tuscan Holdings Corp. | 200.0 | 1 | 100% | March 5, 2019 |

| 10 | Tortoise Acquisition Corp. | 225.0 | 0.5 | 100% | March 1, 2019 |

| Average | 203.7 | 0.55 | 100% |

It’s as if everyone has come to some sort of consensus that ~$200 to $250 million with 1/2 warrant and 100% in trust is what works right now, but it’s not without forethought….As we all know, the IPO ultimately takes a backseat to the de-SPACing transaction, which is where the real magic happens. And if past precedent is any indication, it’s far easier to start smaller and raise money later (if you need it) via a PIPE. We haven’t seen a SPAC in the $400-$600 million range in awhile now. A smaller size gives a team a much wider universe of targets and also gives a target company (at de-SPACing) the opportunity for “real institutional investment” via the PIPE.

However, while SPACs have had the good fortune in 2019 to have had an abundance of good teams, and hence, we’re seeing Tier-1-ish terms across the board, this is ultimately not good for SPACs. We need variety to establish which teams truly do command “Tier-1” status and more importantly, to properly evaluate opportunity. They can’t ALL be successful, so how are investors supposed to evaluate? But speaking of evaluating SPACs, given both Vantage Energy (VEAC) and Saban Capital (SCAC) opting to liquidate, shouldn’t that be factored into the terms equation? Because those deals (which were big, tier-1 deals) would appear to be being ignored in the current calculus. Yet even more pressing is, if every SPAC is being factored in as actually BEING successful, what does that do to yields and the SPAC product structure going forward? Too much of a good thing is….not good.

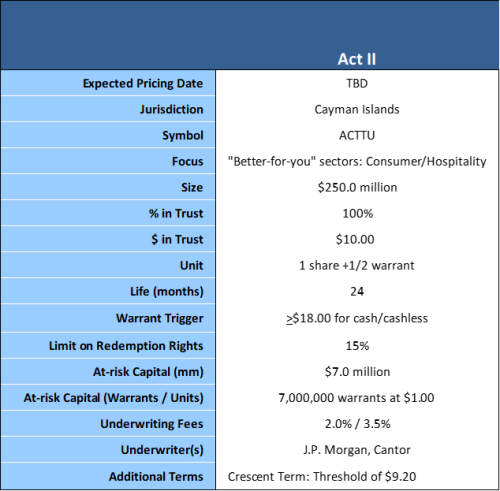

Nevertheless, Act II is interesting for completely different reasons. For one, J.P. Morgan is lead underwriter and we haven’t seen J.P. Morgan involved in a SPAC since 2017. In 2017, JPM underwrote TPG Pace Holdings Corp (TPGH), Capitol Investment Corp IV (CIC), Mosaic Acquisition Corp. (MOSC) and Regalwood Global Energy Ltd. (RWGE). Yet, never from the left lead position. However, they do have Cantor as their co-lead underwriter and Cantor has a ton of SPAC experience and is frankly, one of the more commercial underwriters. They know what will sell. Having said that, let’s take a closer look at this SPAC.

Act II Global Acquisition Corp.

Act II is being led by Irwin D. Simon, as Executive Chairman of the Board. Mr. Simon, who founded The Hain Celestial Group, Inc. (NASDAQ: HAIN), is easily the most notable operator in the “Better-For-You” stated sector focus of this SPAC. Additionally, John Carroll, who is the CEO of Act II, was most recently Executive Vice President Global Brands, Categories and New Business Ventures of Hain Celestial. As for this SPAC’s focus, the “Better-For-You” sector, which focuses on health and wellness, is clearly very modern and potentially very appealing to investors.

However, what I found notable about this team is the addition of an investor relations professional via Mary Celeste Anthes. Off the top of my head, I can’t remember any other teams utilizing a roster this way, but it makes sense. The hardest part of the de-SPACing is the marketing. So the fact that a team has already built in that capability is nice check mark in that column.

Additionally, the prospectus touts Anish Gupta as having the always attractive “prior SPAC experience”, having worked on the Matlin & Partners transaction with U.S. Wells Services (USWS). However, Mr. Gupta was not part of the IPO SPAC team, rather, he was an advisor to the de-SPACing. That’s still great SPAC experience, but it’s still not “SPAC team experience”. Regardless, Mr. Gupta has had a front row seat to SPAC negotiations and that will certainly be advantageous when it comes time for Act II to negotiate their own deal.

All told, Act II is yet another good looking SPAC. Ironically, if this SPAC debuted last year at this time, it probably would have made more of a splash. Unfortunately, right now, it’s one of many of a similar caliber. It begs the question…how do you stand out in this kind of a SPAC market??

Summary of terms below:

With the passage this weekend of $95 billion in funding for Ukraine, Israel and Taiwan by the House of Representatives, some focus has gone back towards the defense sector, which has generally had a good year as a whole. But, SPACs have not been as active in defense, despite the fact that companies in the...

At the SPAC of Dawn As April’s sleepy month for SPAC news continues, there is only one special meeting on the docket to consider a SPAC deal approval, that being today’s vote on Pegasus Digital Mobility‘s (NYSE:PGSS) combination with equipment manufacturer Schmid. Three more SPACs are facing extension votes this week, including Pyrophyte (NYSE:PHYT), whose...

Terms Tracker for the Week Ending April 19, 2024 Welcome to our weekly column where we discuss the findings from our IPO terms tracker based on the previous week’s pricings. Passover and school spring break starts next week, which most likely means a slowdown in SPAC filing activity. Although Churchill IX is now rumored to...

Despite a week of general pull-backs in the market, fintech firm Ibotta (NYSE:IBTA) nonetheless took the dive and had a good week debuting via a traditional IPO in the choppy waters. The company, which provides app-based consumer cashback discounts on purchases, priced its IPO at $88, above its proposed range of $76 to $84, and...

At the SPAC of Dawn Happy Friday! SPACInsider has unveiled new presets on SPAC Performance accessible via the Data drop-down to easily sort for the highest and lowest performing active SPACs and de-SPACs. On the de-SPAC side, Vertiv (NYSE:VRT) continues to be well ahead of the pack, logging a 710% return by share price adjusted...